(Editor's note: this is a syndicated article from Crunchbase News, written by research lead Gené Teare)

As we look at the current economic situation and try to navigate what’s ahead, an analysis of the 2008 downturn and how that impacted funding proves helpful. In an effort to help our readers put what’s happening today into context, we jumped aboard an analytical time machine set for 2008 when investors were sounding strong alarms to their venture-backed companies.

At the time, such investors were telling companies to assess their runway and get profitable toward the end of the third and beginning of the fourth quarter in 2008.

To put it bluntly, Sequoia warned startups to “Get Real or Go Home.”

The collapsing stock market in 2008, in the wake of the subprime mortgage crisis, triggered these warnings. And in September 2008 Lehman Brothers (the fourth-largest investment bank in the U.S.) collapsed.

Walking it back

Unlike the 2000 dotcom crash, the 2008 financial crisis did not start in tech.

Kara Swisher, then founder of AllThingsD, captured the paradox in Irony Alert: Bubble-Making Venture Capitalists Start Popping Them, with venture firms popping their own bubbles, having caused the prior bubble in 2000.

Om Malik reported on the “Sequoia RIP Good Times meeting” with portfolio companies. At the time, one assessment was that the downturn could impact us for a long time to come, as much as 17 years from previous cycles. Another sentiment was that raising funding without being cash flow positive would be hard.

At that time, Jason Calacanis – now founder of Launch – wrote in his post (The) Startup Depression: “50-80% of the venture-backed startups currently operating will shut down or go on life-support.”

What this means today

Investors then–and now–quickly turned inward to assess their existing portfolio companies’ health to create strategies for those who have shorter runways and would need to cut back. Today, as then, companies are advised to plan for two years without raising new funding. All startups have to throw out previous business plans, reassess expenses, sales projections and risks.

Tomasz Tunguz of RedPoint wrote recently about what the venture market could look like in the coronavirus era.

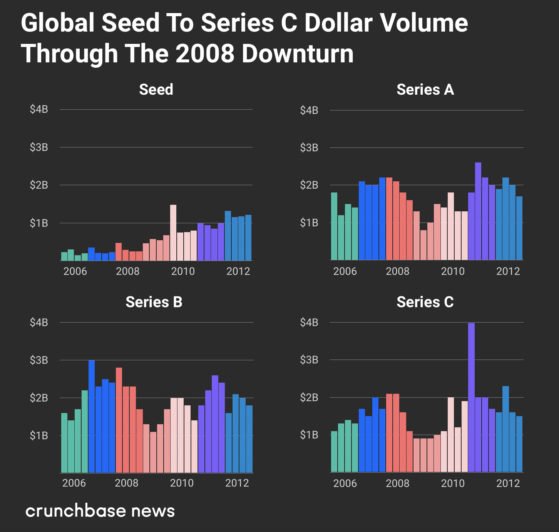

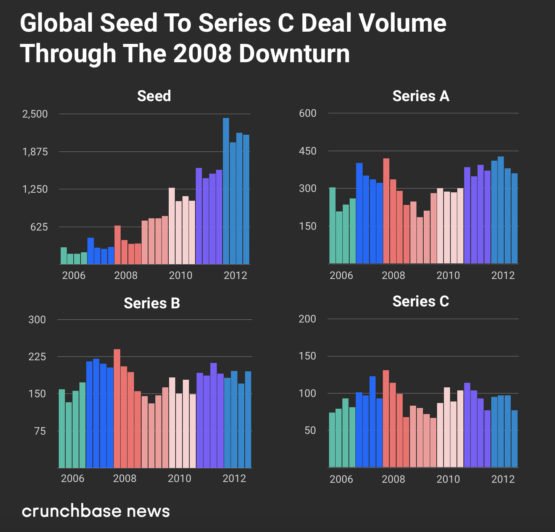

Below we look at the same time period from Crunchbase global data to review early-stage funding trends from 2006 to 2012.

From our analysis, seed-stage rounds were the least impacted of all the early-stage rounds. Seed dollars grew in 2008, 2009 and 2010.

Why would this be the case when early-stage funding, especially for new companies, would be expected to slow down? We can hazard a guess that at the time seed was growing as a new institutional funding class due to the innovation in cloud (Amazon Web Services launched in 2006) and mobile (iPhone launched in 2007). The first trend made it far cheaper to launch a company, hence the growth of seed, and the second created a new wave of technology, establishing unique business opportunities.

Early-stage funding cuts

The funding environment shifted dramatically for Series A, B and C rounds in 2009 down year over year by 40 percent, 41 percent and 46 percent, respectively. The lowest quarter for Series A and B was the second quarter in 2009 and for Series C the third quarter. In 2010 the funding market started growing again, but it took until 2011 for Series A and C round amounts to reach above the volume of invested dollars in 2007.

Global funding counts

Seed counts grew year over year. The slowest growth was the 2009 year post crash with 29 percent growth year over year. The following years, 2010, 2011 and 2012, all grew by more than 50 percent year over year.

A, B and C round counts in 2009 were down between 27 and 28 percent year over year. That means one-third fewer startups raised early-stage funding in 2009. Funding round counts grew in 2010. Series A round counts rose above 2007 levels in 2011, Series B in 2013 and Series C in 2014.

Conclusion

The crisis this time around is very different. Business suspensions and closures have been dramatic as shelter-in-place orders have been set worldwide. Global travel is disrupted. Nonessential retail businesses have been closed. Manufacturing and construction are all closed down except essential functions.

Elon Musk got knuckle-rapped for continued Tesla manufacturing despite the shelter-at-home order in Silicon Valley. The ramifications for society are widespread with daily mounting unemployment figures. The length of shelter-in-place in our communities will impact the longevity of this crisis.

The venture and tech industry have also changed quite dramatically since 2008, with more than sixfold expansion, and technology more integrated in our daily lives.

A week ago Joanna Glasner from Crunchbase news reported we have not seen a dip in funding … yet. We will continue to report on this in the months to come.

Methodology

- Seed/Angel include financings that are classified as a seed or angel, include venture rounds without a designated series that are below $3 million.

- Please note that all funding values are given in U.S. dollars unless otherwise noted. Crunchbase converts foreign currencies to U.S. dollars at the prevailing spot rate from the date funding rounds are reported.

Illustration: Dom Guzman

Would you like to write the first comment?

Login to post comments