Editor’s note: This is a sponsored article, written by Philippe Botteri, a partner at VC firm Accel, as a follow-up to earlier guest posts on their annual list of the top 100 SaaS companies in the European SaaS startup industry, with the help of Varun Purandare and Candice du Fretay.

The Accel 2020 Euroscape was unveiled earlier today at SaaStockEMEA and the full slideshow is available here. You’ll also find the video recording of the presentation at the end of this article. We’d like to thank KeyBank and G2 for providing some of the data used in the report.

It’s an amazing time to be a cloud entrepreneur in Europe. It reminds me of living in Silicon Valley 10 years ago when so many foundational SaaS companies were started. The European cloud ecosystem is growing much faster than anyone could have anticipated: last year, we predicted that it would take another three years for Europe to generate its first decacorn. UiPath broke that milestone this summer, in just nine months, establishing Europe as a major global center for software innovation.

This year, in addition to unveiling the Euroscape, our list of top 100 Cloud companies started in Europe and Israel; and our Champions League, the high-growth unicorns from the region; we’ll also unveil the Accel Euroscape Public Index, the index of the European and Israeli-born public cloud companies, and its performance.

Before jumping into the list, let’s have a quick look at what’s been a very special year in many ways for the cloud ecosystem globally and in Europe.

A New Software Era: The Rise of the Giants

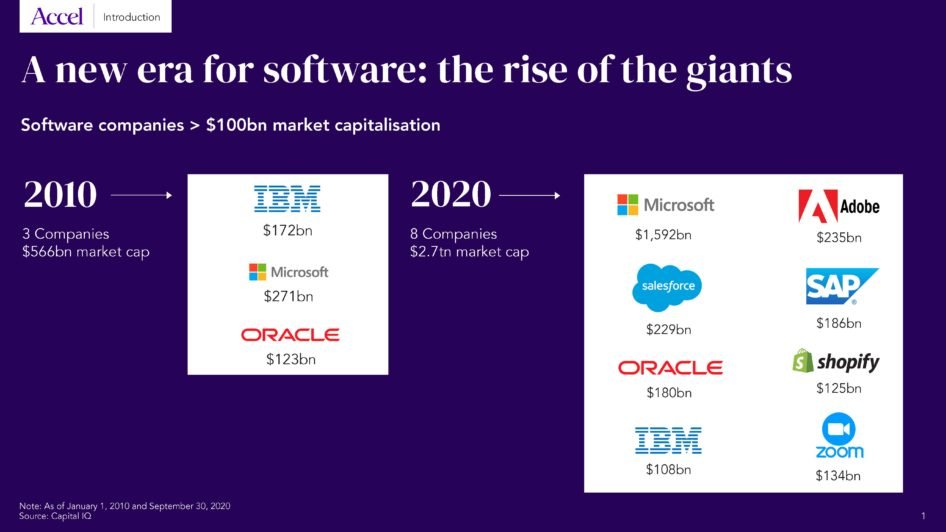

Software has been eating the world for 30 years now, but looking at the acceleration we have seen in the past decade, software has entered a new era: “the rise of the giants”. There are now eight software companies north of a $100 billion market cap, representing $2.7 trillion of market value. This is a big jump vs. 2010 when we only had three companies (Microsoft, Oracle and IBM) valued just over $550 billion. What’s even more impressive is the new generation, with 75 public cloud companies valued above $1 billion vs eight companies in 2010 and 26 of these companies are already above $10 billion.

If we zoom out and look at the overall cloud market, we can see momentum building. The Cloud market tripled in the past five years to reach $100 billion today and if its growth continues at a similar pace, we estimate that Cloud will overtake on-premise software by 2025, when the entire software market should be worth around $1 trillion.

Europe has also joined the race with its first Cloud giants. This summer saw two record transactions within a month, as UiPath became the first European Cloud decacorn in July and Visma, a Norwegian company, became the world’s largest ever software buyout with a $12B+ valuation. Big milestones for the old continent!

Cloud Entrepreneurs: Embracing the “Silicon Valley State of Mind”

Accel has been a big believer in cloud since the early days of this secular shift. We've invested $5B+ in more than 250 companies and feel privileged to have partnered with category-defining companies such as Atlassian, Crowdstrike, Docusign, Dropbox, Slack and UiPath.

And Europe has shown even greater acceleration. We've increased our investments five-fold in the last five years, backing close to 50 cloud companies of which seven have already become unicorns.

Looking at the map above, it’s so inspiring to see Cloud entrepreneurs across the globe. The one thing that unites them all is their ambition to make a global impact and change the world - the “Silicon Valley state of mind”.

2020 Cloud Market: Is The Sky the Limit?

The momentum of Cloud companies is also seen in the public markets. It seems unstoppable with around $1 trillion of value created in the past 12 months and the Cloud Index massively outperforming the Nasdaq. This unprecedented growth is driven by the acceleration of digital transformation and an increase in valuation multiples which have reached historic heights. The average revenue multiple is now 17x+, close to 10 times higher than during the 2008 crisis! Is the sky the limit for Cloud public stocks?

On the IPO front, the one word that comes to mind is “supersize”.

While the number of IPOs in 2020 is close to 2019, the average valuation has doubled compared to last year, driven in particular by the massive IPO of Snowflake, which reached a $70 billion market cap on its first trading day. And public companies have also taken advantage of the favourable market environment to raise 2x more capital than they did last year through secondary offerings and convertible bonds.

And what about Europe?

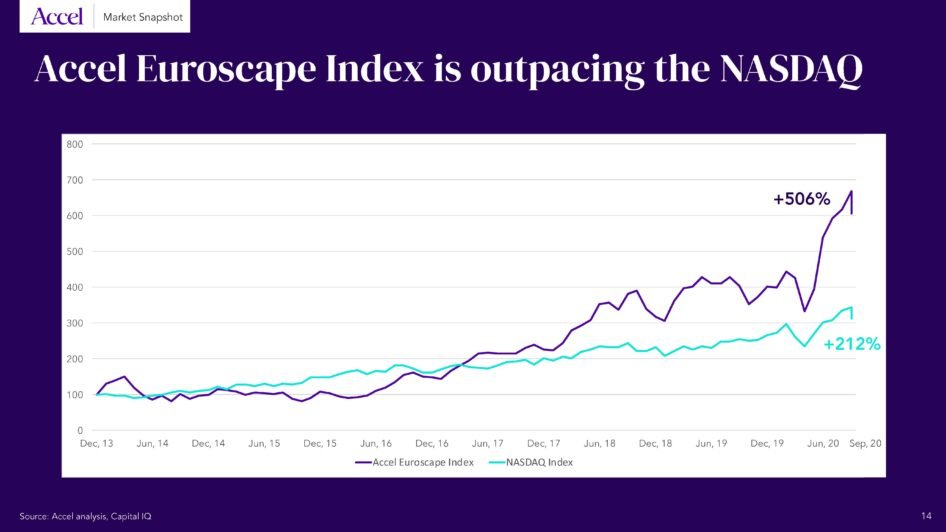

When I started in venture, I was fortunate to witness the birth of the first generation of cloud companies in the US. This led me to launch the SaaS 13 Index in February 2008 while I was at Bessemer. It consisted of 13 companies and in 12 years has evolved into a massive Index representing $1.7 trillion in market cap. Today, we’ve reached the point where Europe deserves its own Index, and we’re very happy to announce the creation of the Accel Euroscape Public Index, the Index of public cloud companies born in Europe and Israel.

It’s composed of 10 flagship companies with a combined value close to $100 billion: Elastic, Dynatrace, JFrog, Mimecast, Talend, TeamViewer, Unity, Varonis, Wix and Zendesk. Since 2013, when Wix, the first of these companies went public, the Euroscape Public Index has outpaced the Nasdaq by 2.5x, achieving more than 500% growth in seven years.

We expect the growth of the Index to only accelerate as Europe generates more unicorns. In 2020, Europe and Israel minted seven new unicorns, taking the total number to 25.

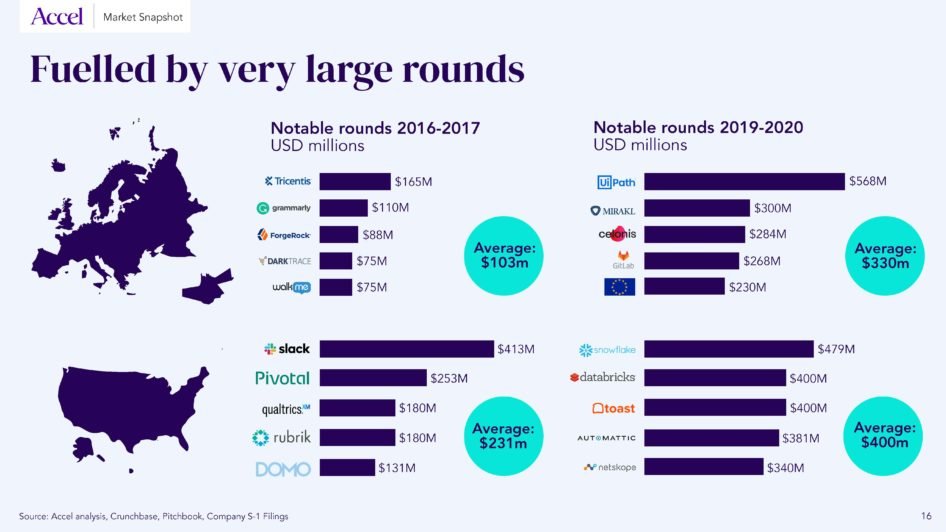

This growth has been fuelled by much larger private investment rounds. In 2016-17, the five largest rounds had an average size of $100 million. In 2019-20, this number has grown to $330 million. Europe is catching up with the US, which is very exciting!

However, it’s not only about a few large rounds. The entire amount invested in private cloud companies in Europe and Israel in 2020 has grown close to 30% so far to $9-9.5 billion, which is nearly half the c. $20 billion invested in US-born cloud companies.

Accel 2020 Euroscape and Champions League

Before unveiling the Euroscape and Champions League, we wanted to highlight a couple of facts showing how far the EU cloud ecosystem has come. First, from a funding perspective, the 2020 Euroscape winners, including the Champions League, have raised a whopping $14 billion. That’s close to 6x more than in 2016. Secondly, these companies have created more than 70,000 jobs, and the unicorns emerging represent around $60 billion of market cap, which is half of the value of the Euroscape Public Index!

To develop the list, we surveyed more than 1,500 European and Israeli private SaaS companies across 20 countries and a number of categories. We’ve made a couple of changes to the list this year as well, adding payments as a new category and only including unicorns in the Champions League.

The 2020 Champions League

This year, the list is comprised of 19 category-defining companies from 12 cities and nine countries. Their average employee growth in the past 12 months was north of 40% and they’ve raised $6.7 billion of combined funding. An impressive list! It’s incredible to see what Europe has been able to generate.

And now, for the Accel Euroscape 2020! We must say that it was incredibly hard to put the list together this year as we had so many great applicants. As you can see, both the data and security categories are booming, and we welcome the addition of payments and banking infrastructure fueled by the expansion of a new generation of financial services.

What’s very exciting for us is that these 100 companies come from 34 cities and 21 countries, showing that success can come from anywhere in Europe.

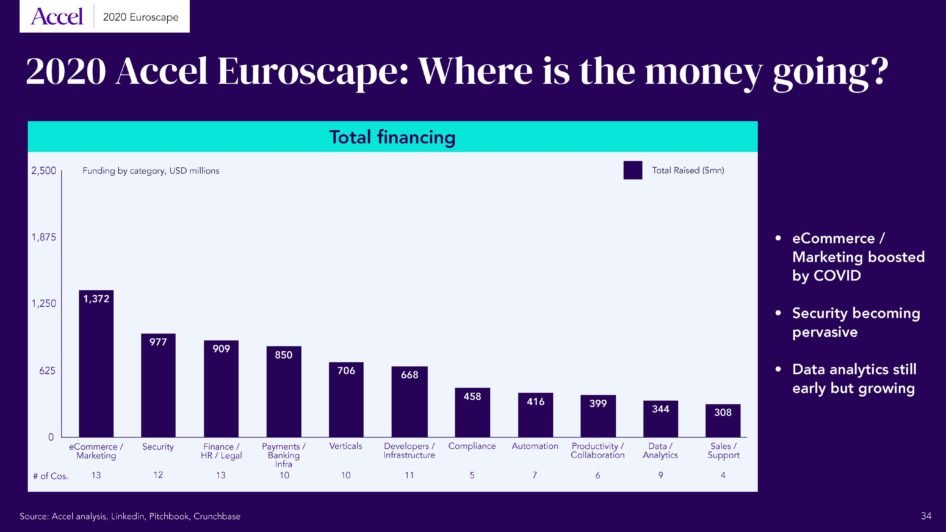

With $7.4 billion in funding raised by the winners, it’s interesting to look at where the money has been directed. We can see e-commerce/marketing has been boosted by COVID and security is in second place, with cyber criminality not slowing down. The data analytics category is showing early promise with many companies in the space.

You'll find more analyses on the 2020 winners in the full presentation

A strange year: It was the best of times, it was the worst of times…

While many lights are green, it’s hard to ignore the fact that COVID-19 has changed the lives of billions of people. In 2000 and 2008, the economic crises had a dramatic impact on the tech ecosystem, but 2020 seems to be very different. Let’s take a look at how cloud companies have been impacted by the pandemic.

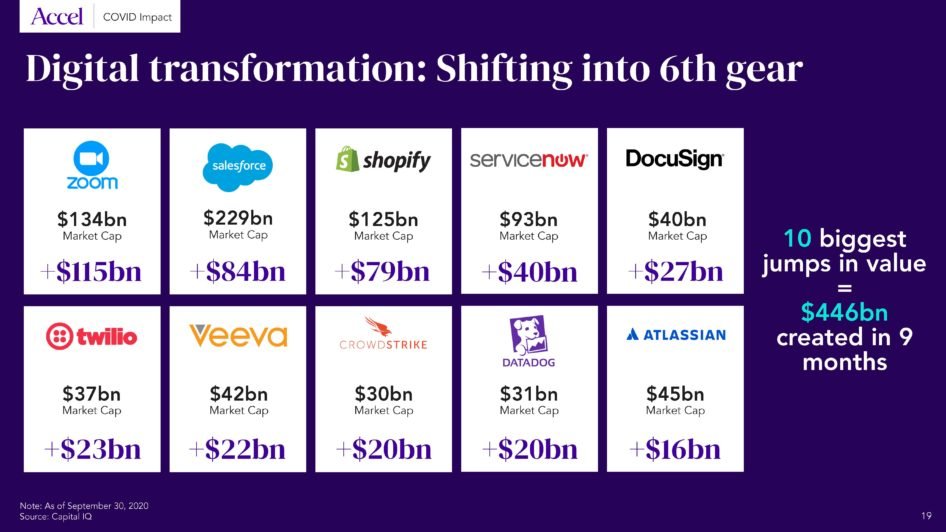

The first impact of COVID has been to radically transform the work from home paradigm and massively accelerate digital transformation – by at least two years. Ten public cloud companies have hugely benefited from this acceleration, Zoom being the first. Together, these ten companies have seen an increase of their market value by close to $0.5 trillion, representing half of the increase in value of the global cloud Index in just nine months.

That said, this impact has been fairly concentrated. Overall, cloud spending growth in Q2 was in line or even slightly below the historical average.

On the private company side, the impact of COVID falls into three buckets:

- Roughly 20% of the companies have seen strong acceleration, particularly companies in collaboration, e-commerce, automation and security - Most companies saw a moderate to limited impact - A few companies selling into distressed sectors like travel or hospitality have been severely impacted

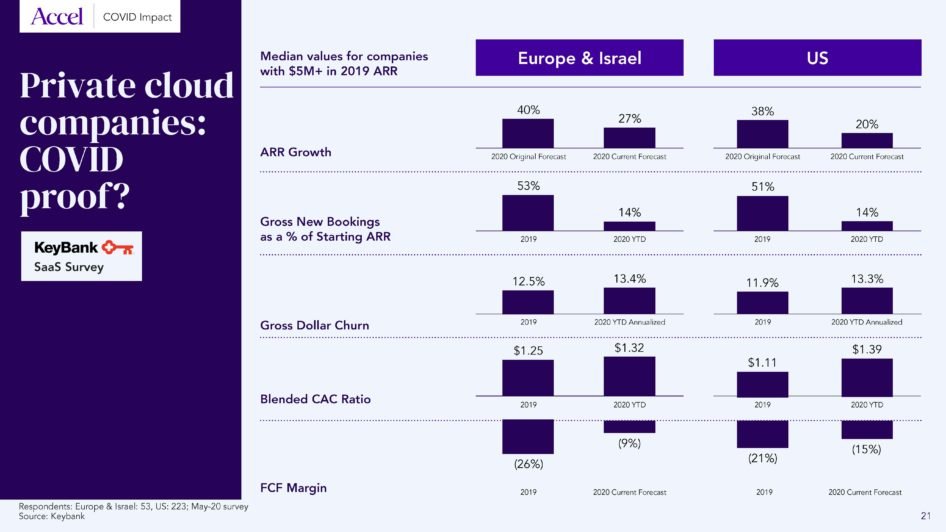

If we look at the survey performed by KeyBank, it’s very much in line with what we have observed in our portfolio. Overall, COVID-19 prompted people to revise their growth forecast slightly downward and be more conservative on their cash burn, but so far, the impact hasn’t been dramatic. Interestingly, companies have adapted very similarly in Europe and the US, except on the cash front, where EU companies have been more conservative.

This crisis is very different from what we’ve seen in the past, as there are as many opportunities for cloud companies as there are risks. Navigating this crisis is not about cutting back: it’s about taking advantage of the opportunities while not leaning too far over your ski tips to avoid a catastrophic fall.

I’m sure everyone remembers how hectic March and April were this year. It was frantic but also inspiring as many cloud companies looked beyond their internal challenges and did everything they could to help. For example, I can’t forget the call I had with Stan, Founder and CEO of Doctolib, when he announced that he was shifting the company’s focus to telemedicine to help the French and German healthcare systems during the lockdown. In two weeks, Doctolib made the product self-serve and extensively deployed the solution, which you can hear more about in the short video below.

UiPath was another inspiring company. The founders refocused their foundation to help fight COVID in Romania, achieving a massive impact. I will let Alexandra Dines, Chair of the foundation, tell you more about their story.

What’s Next?

To conclude, let’s have a look at what’s ahead for the cloud ecosystem in Europe. We see five defining trends:

Work coming home: No surprise here. The world of work has changed dramatically, with entire companies moving fully remote as countries were shutting down. With work moving into the home, the need to stay connected dramatically accelerated the need for collaboration tools like Miro, Slack and Zoom. For example, the number of daily meeting participants grew from 10 million in December 2019 to 300 million in April 2020. In addition, entirely new software categories are being created in a record time, like virtual events, a market created by Hopin.

Doctors now online: COVID put the healthcare system under immense pressure in many countries. When physically meeting a medical practitioner became difficult, telemedicine services exploded. In France, Doctolib saw the number of video conferences on their platform grow from 100,000 in the 13 months before lockdown to 4.6 million today. As doctors are embracing new technologies, we think this is only the beginning of the digital transformation of medical practices and hospitals, and we expect a lot more innovation in this vertical in the coming years.

Hyperautomation - Bots and citizen developers transforming the Enterprise: Most people in the world use software, but fewer than one percent can code. It is as if 99% of the world could read but only 1% could write. The emergence of low code/no code platforms is changing this paradigm, enabling a growing number of employees to automate their business processes. Combined with the rapid rise of RPA automating the data and intelligence layers, we expect Enterprise to hyper-automate in the coming years, leading to the rise of a new generation of cloud services.

Fintech stack moving to the cloud: In the past, the complexity of monolithic banking and payment infrastructure made it difficult for non-financial institutions to develop new services. Today, modern API-first platforms are making it possible for many cloud companies to integrate payments and banking services. We expect this trend to disrupt banks and insurance and to give rise to a new generation of Fintech infrastructure companies.

Cybercriminals feasting on Covid: Hackers took advantage of the disruption generated by COVID and made the need for security even more acute. As their environments get more distributed and the notion of perimeter disappears, we are seeing enterprises moving to zero trust architectures, placing more focus on secure code development and securing their data and communication with privacy and encryption tools. With more funding going into the category, we expect to see the momentum continue.

We predict these trends may well produce the next generation of the Champions League.

The European ecosystem has grown so much over the past five years, and it’s been a privilege to be part of it. On behalf of the Accel team, we’d like to congratulate all the champions and top 100 winners and to thank all the cloud founders who have worked hard and had the vision and ambition to make this happen.

As Thomas Edison said, ‘Genius is 1% inspiration and 99% perspiration’. We’ve been very impressed by both the creativity and resilience of the European cloud founders and look forward to meeting a lot more of you in the future!

Feel free to reach out, we’d be happy to hear your story.

Would you like to write the first comment?

Login to post comments